Your offer letter says Rs. 12 LPA. Your first payslip shows Rs. 78,000. That gap is not a mistake. CTC (Cost to Company) and in-hand salary are calculated very differently, and understanding the difference stops a lot of payroll confusion for both employees and HR teams.

This guide explains every component of a CTC structure, what gets deducted before the salary hits the bank account, and how Bangalore-specific deductions like Professional Tax affect the final take-home amount.

Key Takeaways

- CTC is the total cost the employer bears for an employee, including components never paid directly.

- In-hand (take-home) salary is typically 65% to 75% of CTC after all deductions.

- Basic salary is usually 40% to 50% of CTC and drives PF and gratuity calculations.

- Karnataka Professional Tax (max Rs. 200/month) is an additional deduction specific to Bangalore employees.

- Employer PF contribution (12% of basic) is part of CTC but never appears in the employee's bank account.

- TDS under Section 192 is deducted monthly based on projected annual income and tax regime chosen.

What Is CTC (Cost to Company)?

CTC is the total amount an employer spends on an employee in a year. It includes the employee’s direct salary, all allowances, employer-side statutory contributions, and benefits like insurance and gratuity provisioning.

⚠️ Important

CTC is not the amount credited to the employee’s bank account. It is an accounting figure that shows the full cost of employing that person. Several CTC components go directly to government accounts (like PF) or accrue over time (like gratuity) and are never paid as monthly cash.

What Is In-Hand or Take-Home Salary?

In-hand salary (also called take-home pay) is the amount actually credited to the employee’s bank account each month after all deductions. These deductions include employee PF contribution, ESI (if applicable), Professional Tax, and TDS on salary.

💡 Bangalore Benchmark

For most employees in Bangalore, in-hand salary falls between 65% and 75% of CTC. The exact percentage depends on the CTC structure, the employee’s tax regime, and applicable statutory deductions.

CTC Breakup: Every Component Explained

1. Basic Salary

Basic salary is the foundation of your CTC. It is typically 40% to 50% of total CTC. Basic salary is fully taxable and determines two important calculations: PF contribution (12% of basic) and gratuity eligibility.

For a Rs. 12 LPA CTC, basic salary is usually set between Rs. 4.8 LPA and Rs. 6 LPA, or Rs. 40,000 to Rs. 50,000 per month.

2. House Rent Allowance (HRA)

HRA is typically 40% to 50% of basic salary. Employees living in a rented house can claim HRA exemption under Section 10(13A) of the Income Tax Act. The exempt portion depends on actual rent paid, HRA received, and city. Bangalore qualifies as a metro city for HRA exemption purposes.

Employees not living in rented accommodation cannot claim the exemption and the full HRA amount becomes taxable.

3. Special Allowance

Special allowance is the balancing component in most salary structures. It fills the gap between basic plus HRA and the total gross salary. It is fully taxable with no exemption. Some employers split this into multiple named allowances (conveyance, transport, etc.) but the tax treatment is similar.

4. Performance Bonus / Variable Pay

Variable pay is a portion of CTC paid based on individual or company performance. It is typically 10% to 20% of CTC for most roles and higher for sales functions. Variable pay is usually paid quarterly or annually and is fully taxable in the year of receipt.

5. Employer PF Contribution (12% of Basic)

The employer contributes 12% of the employee’s basic salary to the Employees Provident Fund every month. This amount is part of CTC but is deposited directly into the EPFO account. The employee never sees this as cash.

Of the employer’s 12%, 8.33% goes to EPS (Employee Pension Scheme) subject to a maximum of Rs. 1,250 per month, and 3.67% goes to EPF.

6. Gratuity Provision

Gratuity is payable after 5 years of continuous service under the Payment of Gratuity Act. Employers include a monthly gratuity provision in CTC to account for this future liability. The standard formula used for CTC costing is: (Basic / 26) x 15 x (1/12) per month.

This provision is part of CTC but the employee only receives it at exit, after completing 5 years. It is not paid monthly.

7. Medical Insurance

Many employers include group health insurance as part of CTC. The premium paid by the employer is a CTC component but is not cash in hand. The value shown in the CTC letter is the annual premium allocated to that employee.

Monthly Deductions That Reduce In-Hand Salary

| Deduction | Amount | Notes |

|---|---|---|

| Employee PF (12% of basic) | Rs. 4,800/month (on Rs. 40,000 basic) | Goes to EPFO account, not bank |

| Professional Tax (Karnataka) | Rs. 200/month (Rs. 300 in February) | Applicable to all employees earning above Rs. 15,000 gross |

| ESI (0.75% of gross) | Applicable if gross is below Rs. 21,000 | Goes to ESIC; provides medical coverage |

| TDS on Salary | Varies by income and tax regime chosen | Deducted under Section 192; based on annual projection |

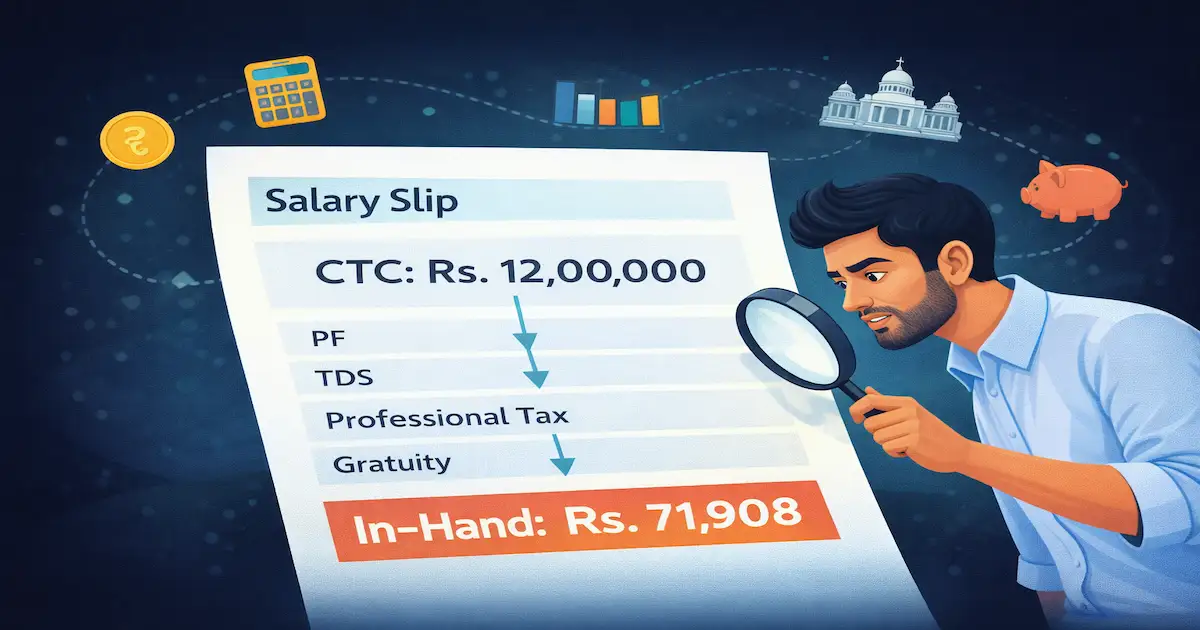

CTC vs In-Hand Salary: A Practical Bangalore Example

This example shows how a Rs. 12 LPA CTC translates to an in-hand salary for a Bangalore employee under the old tax regime.

| CTC Component | Annual (Rs.) | Monthly (Rs.) |

|---|---|---|

| Basic Salary (40% of CTC) | 4,80,000 | 40,000 |

| HRA (50% of basic) | 2,40,000 | 20,000 |

| Special Allowance | 2,54,400 | 21,200 |

| Performance Bonus | 96,000 | 8,000 |

| Employer PF (12% of basic) | 57,600 | 4,800 |

| Gratuity Provision | 27,693 | 2,308 |

| Medical Insurance Premium | 18,000 | 1,500 |

| Gross CTC | 12,73,693 | 1,06,141 |

| Less: Employee PF (12% of basic) | -57,600 | -4,800 |

| Less: Professional Tax (Karnataka) | -2,500 | -200 (avg) |

| Less: TDS (estimated, old regime) | -50,000 | -4,167 |

| In-Hand / Take-Home Salary (approx) | 8,62,900 | 71,908 |

In this example, a Rs. 12 LPA CTC results in approximately Rs. 71,908 per month in-hand. The effective take-home is about 67% of CTC. The actual figure will vary based on the tax regime chosen, actual rent paid, and investment declarations under Section 80C.

💡 How the Calculation Works

Step 1: CTC minus Employer PF and Gratuity = Gross Salary

Step 2: Gross Salary minus Employee PF (12% of basic) = Taxable Salary

Step 3: Taxable Salary minus PT (Karnataka) = Net before TDS

Step 4: Net before TDS minus TDS (as per regime) = In-Hand Salary

Result: In-hand is typically 65% to 75% of CTC for Bangalore employees

Calculate Your Exact In-Hand Salary from CTC

Use the free Bangalore Salary Calculator to see your take-home after PF, PT, and TDS deductions.

New Tax Regime vs Old Tax Regime: Impact on In-Hand Salary

The choice of tax regime significantly affects monthly TDS deductions and therefore the in-hand salary.

Under the new tax regime (default from FY 2023-24), lower tax rates apply but most exemptions and deductions (HRA, 80C, 80D) are not available. Under the old regime, higher rates apply but exemptions like HRA and Section 80C investments reduce taxable income.

For employees with significant HRA exemption (paying high rent in Bangalore) and active 80C investments, the old regime often results in lower TDS and higher take-home. For employees with minimal exemptions, the new regime is typically better.

HR Software Bangalore allows employees to declare their regime choice during investment declarations. The system adjusts monthly TDS deductions automatically based on the regime selected. Learn more about our payroll software for Bangalore businesses.

Frequently Asked Questions

CTC includes components that are never paid as cash: employer PF contribution (12% of basic), gratuity provisioning, and insurance premiums. On top of that, employee-side deductions (employee PF, PT, TDS) reduce your gross salary further. The gap between CTC and in-hand is typically 25% to 35%.

A higher basic salary increases PF contribution (both employee and employer sides), which builds retirement savings but reduces monthly take-home. It also increases gratuity payout over time. A lower basic with higher special allowance gives more monthly cash but lower long-term benefits.

HRA exemption in Bangalore (a metro city) is the least of three values: actual HRA received, 50% of basic salary, or actual rent paid minus 10% of basic salary. Only the exempt portion is tax-free. The rest is taxable. Employees must submit rent receipts or a rental agreement to claim this exemption.

For employees earning above Rs. 25,000 gross per month in Bangalore, the PT deduction is Rs. 200 per month (Rs. 300 in February). For those earning Rs. 15,001 to Rs. 25,000, it is Rs. 150 per month. Below Rs. 15,000, no PT is deducted.

Use this formula as a starting point: In-hand = CTC minus employer PF minus gratuity provision minus insurance, then minus employee PF, PT, and estimated TDS. For an accurate calculation specific to your CTC structure and tax situation, use the HR Software Bangalore Salary Calculator.

Know Exactly What Your Employees Take Home

HR Software Bangalore calculates CTC breakups, handles PT, PF, ESI, and TDS automatically, and generates accurate payslips every month.